Note

Click here to download the full example code

Holidays from Exchange Calendar¶

busdayaxis.holidays_from_exchange builds the holidays= list automatically

from a real exchange calendar, so you don't have to maintain the dates by hand.

It supports both pandas_market_calendars and exchange_calendars — the

function duck-types the calendar object and picks the right calling convention.

Optional dependency

This example requires pandas_market_calendars::

pip install pandas_market_calendars

exchange_calendars is equally supported:

pip install exchange_calendars

Core code:

import pandas_market_calendars as mcal

cal = mcal.get_calendar("NYSE")

holidays = busdayaxis.holidays_from_exchange(cal, "2025-01-01", "2025-01-31")

ax.set_xscale("busday", holidays=holidays)

import matplotlib.dates as mdates

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import pandas_market_calendars as mcal

import busdayaxis

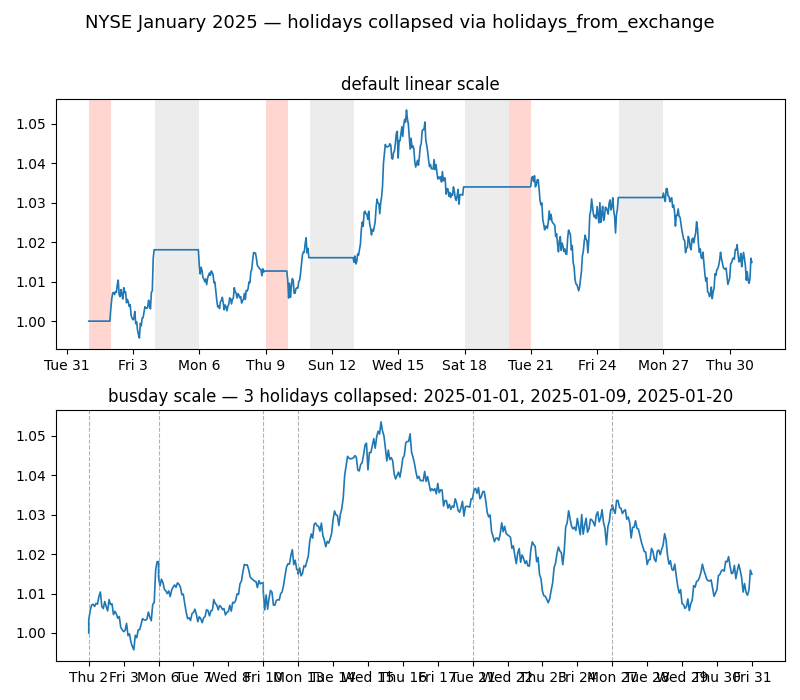

Build the holiday list from the NYSE calendar. January 2025 has two NYSE holidays: New Year's Day (Jan 1) and MLK Day (Jan 20).

cal = mcal.get_calendar("NYSE")

holidays = busdayaxis.holidays_from_exchange(cal, "2025-01-01", "2025-01-31")

Prepare dummy price data for January 2025

dates = pd.date_range("2025-01-01", "2025-01-31", freq="h")

returns = np.random.normal(0, 0.002, len(dates))

returns[~np.is_busday(np.array(dates, dtype="datetime64[D]"), holidays=holidays)] = 0.0

prices = (1 + pd.Series(returns, index=dates)).cumprod()

fig, (ax1, ax2) = plt.subplots(2, 1, figsize=(8, 7), sharey=True)

fig.suptitle(

"NYSE January 2025 — holidays collapsed via holidays_from_exchange", fontsize=13

)

# default linear scale

ax1.plot(dates, prices.values, linewidth=1.2)

ax1.set_title("default linear scale")

ax1.xaxis.set_major_locator(mdates.DayLocator(interval=3))

ax1.xaxis.set_major_formatter(mdates.DateFormatter("%a %-d"))

# shade holidays and weekends on the linear axis

full_days = pd.date_range("2025-01-01", "2025-01-31", freq="D")

for d in full_days:

if d.weekday() == 5:

ax1.axvspan(d, d + pd.Timedelta(days=2), color="grey", alpha=0.15, linewidth=0)

for h in holidays:

ax1.axvspan(

pd.Timestamp(h),

pd.Timestamp(h) + pd.Timedelta(days=1),

color="tomato",

alpha=0.25,

linewidth=0,

label=h,

)

# busday scale with exchange holidays collapsed

ax2.plot(dates, prices.values, linewidth=1.2)

ax2.set_xscale("busday", holidays=holidays)

ax2.set_title(

f"busday scale — {len(holidays)} holidays collapsed: {', '.join(holidays)}"

)

ax2.xaxis.set_major_locator(busdayaxis.DayLocator())

ax2.xaxis.set_major_formatter(mdates.DateFormatter("%a %-d"))

busdayaxis.mark_gaps(ax2, alpha=0.6)

_ = plt.tight_layout(rect=[0, 0, 1, 0.96])

Total running time of the script: ( 0 minutes 0.384 seconds)

Download Python source code: plot_1b_holidays_from_exchange.py

Download Jupyter notebook: plot_1b_holidays_from_exchange.ipynb